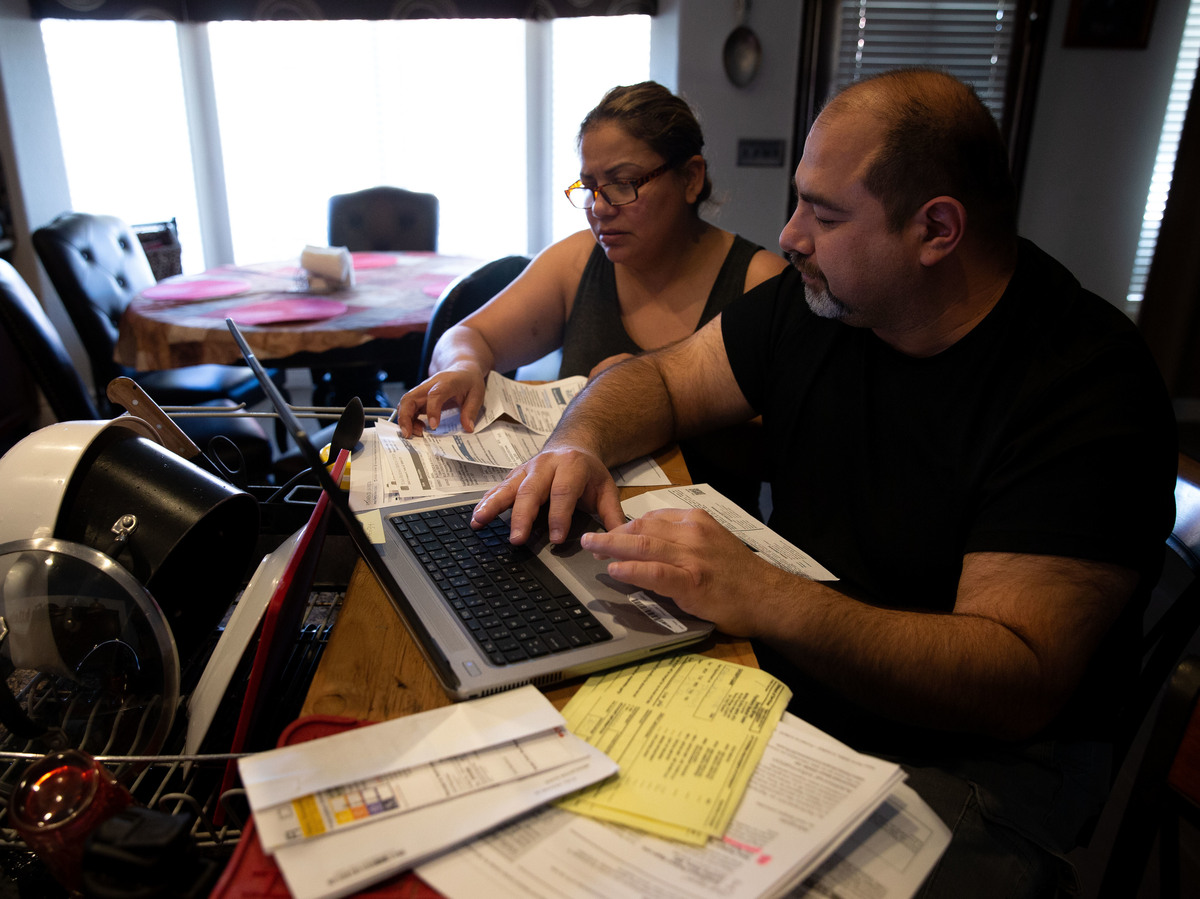

The Fierro family of Yuma, Arizona, had a string of bad medical luck that started in December 2020.

That’s when Jesús Fierro Sr. was admitted to the hospital with a serious covid-19 infection. He spent 18 days at Yuma Regional Medical Center, where he lost 60 pounds. He came home weak and dependent on an oxygen tank.

Then, in June 2021, his wife, Claudia, fainted while waiting for a table at the local Olive Garden. She felt dizzy one minute and was in an ambulance on her way to the same medical center the next. She was told her magnesium levels were low and was sent home within 24 hours.

The family has health insurance through Jesús Sr.’s job. But it didn’t protect the Fierros from owing thousands of dollars. So, when their son Jesús Fierro Jr. dislocated his shoulder, the Fierros — who hadn’t yet paid the bills for their own care — opted out of U.S. health care and headed south to the U.S.-Mexico border.

And no other bills came for at least one member of the family.

The Patients: Jesús Fierro Sr., 48; Claudia Fierro, 51; and Jesús Fierro Jr., 17. The family has Blue Cross Blue Shield of Texas health insurance through Jesús Sr.’s employment with NOV Inc., formerly National Oilwell Varco, a multinational oil company.

Medical Services: For Jesús Sr., 18 days of inpatient care for a severe covid infection. For Claudia, less than 24 hours of emergency care after fainting. For Jesús Jr., a walk-in appointment for a dislocated shoulder.

Total Bills: Jesús Sr. was charged $3,894.86. The total bill was $107,905.80 for covid treatment. Claudia was charged $3,252.74, including $202.36 for treatment from an out-of-network physician. The total bill was $13,429.50 for less than a day of treatment. Jesús Jr. was charged about $5 (70 pesos) for an outpatient visit that the family paid in cash.

Service Providers: Yuma Regional Medical Center, a 406-bed, nonprofit hospital in Yuma, Arizona. It’s in the Fierros’ insurance network. And a private doctor’s office in Mexicali, Mexico, which is not.

What Gives: The Fierros were trapped in a situation that more and more Americans find themselves in: They are what some experts term “functionally uninsured.” They have insurance — in this case, through Jesús Sr.’s job,